Nina Mohanty made her mark in some of the UK’s most recognisable finance companies, including Mastercard, Starling Bank and Klarna.

However, her personal experience growing up in the US as the daughter of immigrants, and later as a newcomer navigating the UK’s financial system, ultimately inspired her to build her own purpose-led business.

In 2021, Mohanty founded Bloom Money – a fintech startup that digitises traditional savings methods, helping immigrant communities in the UK build financial resilience. We’re proud to say that Bloom Money was formed with 1st Formations, and Nina continues to use our support services today as she grows her business.

What sets this story apart from others in the fintech space? Inside Bloom Money lies generations of stories – of immigrant identity, diaspora and the beauty of community – that go far beyond financial innovation. We recently sat down with Mohanty to discover her story and why Bloom Money serves as both a call to action for other purpose-driven founders and a challenge to financial systems.

Key takeaways

- Bloom Money digitises communal saving circles to offer trusted financial tools for immigrant communities excluded by traditional banks.

- Nina Mohanty’s lived immigrant experience directly shaped a fintech model grounded in cultural understanding and community trust.

- Purpose-led businesses thrive when founders deeply engage with the people they serve and design for real-world cultural contexts.

Why community finance matters – and how it shaped Bloom Money

To appreciate what Bloom Money stands for, it’s important to understand the systems and challenges that inspired it.

According to 2023 research by the UK’s Financial Inclusion Commission, approximately 1.1 million adults (about 2.1% of the UK population) are ‘unbanked’, meaning they don’t have a bank account. Many are immigrants who either can’t access the formal banking system or actively avoid it. People may not have access to banking because they lack the necessary documents. They might also come from places where the overall perception is that banks are corrupt, exclusionary, or don’t accommodate their needs.

Instead of relying on traditional banks, many immigrant and diaspora communities turn to something they know and trust: community-based savings circles.

What are community-based savings circles?

A community-based savings circle – also known as a rotating savings and credit association (ROSCA) or savings club – is a traditional and collaborative way for a group of people to save and access money together.

Here’s how susus, chit funds, hagbad and junta – all names of community-based savings circles – work:

- A group of people, usually friends, family, or community members, form a savings circle

- Each member contributes a fixed amount of money regularly (weekly, biweekly, or monthly)

- One member receives the entire pooled amount each cycle (called a ‘payout’ or ‘hand’)

- This continues until everyone has received a payout once

- After the full cycle, the group can choose to stop or start a new round

For example:

- 10 members each contribute £100 per month

- Every month, £1,000 is collected

- Each month, a different member gets the full £1,000

- Over 10 months, everyone gets £1,000 once – but in a different month

Many communities turn to community-based savings circles because they’re built on mutual accountability and often serve as the only trusted financial safety net.

Financial exclusion and the need for alternatives

Research by Fair4Finance into inclusive access to financial services reveals a troubling picture. In the UK, people from minority ethnic backgrounds face significantly higher levels of financial exclusion. For example, 45% have sought help from a financial provider on issues like setting up an account or transferring money – nearly double the number of white individuals who have done the same (25%).

- Taking the leap to start a business: what makes us hesitate?

- Best time to start a business (UK): Season, tax year & readiness

- Why a superstar hire can change everything

Most concerning of all, the research shows that 1 in 5 people from minority ethnic groups experience racial discrimination when dealing with financial providers.

These barriers help explain why alternative, community-driven approaches to saving persist – and why they matter so deeply.

How personal experience inspired the Bloom Money app

For Nina Mohanty, community-based savings systems aren’t just interesting ideas – they’ve been part of her everyday life. Growing up in California in a mixed-heritage immigrant family, she experienced firsthand the resourcefulness and trust that often define immigrant households.

“I grew up with a lot of immigrant family behaviours,” she recalls, “like scrimping and saving every plastic bag, or the Danish tin that’s never full of biscuits, it’s actually a sewing kit.”

When Nina moved from the US to the UK, she immediately ran into barriers.

I really struggled to open a bank account, and from there I couldn’t get a phone contract because I didn’t have a current account. So, I couldn’t set up a direct debit. I ultimately had to MacGyver my way and figure something out.

That blend of personal experience and professional insight sparked the idea for Bloom Money – a purpose-led fintech built to serve people where they are, not where the system expects them to be.

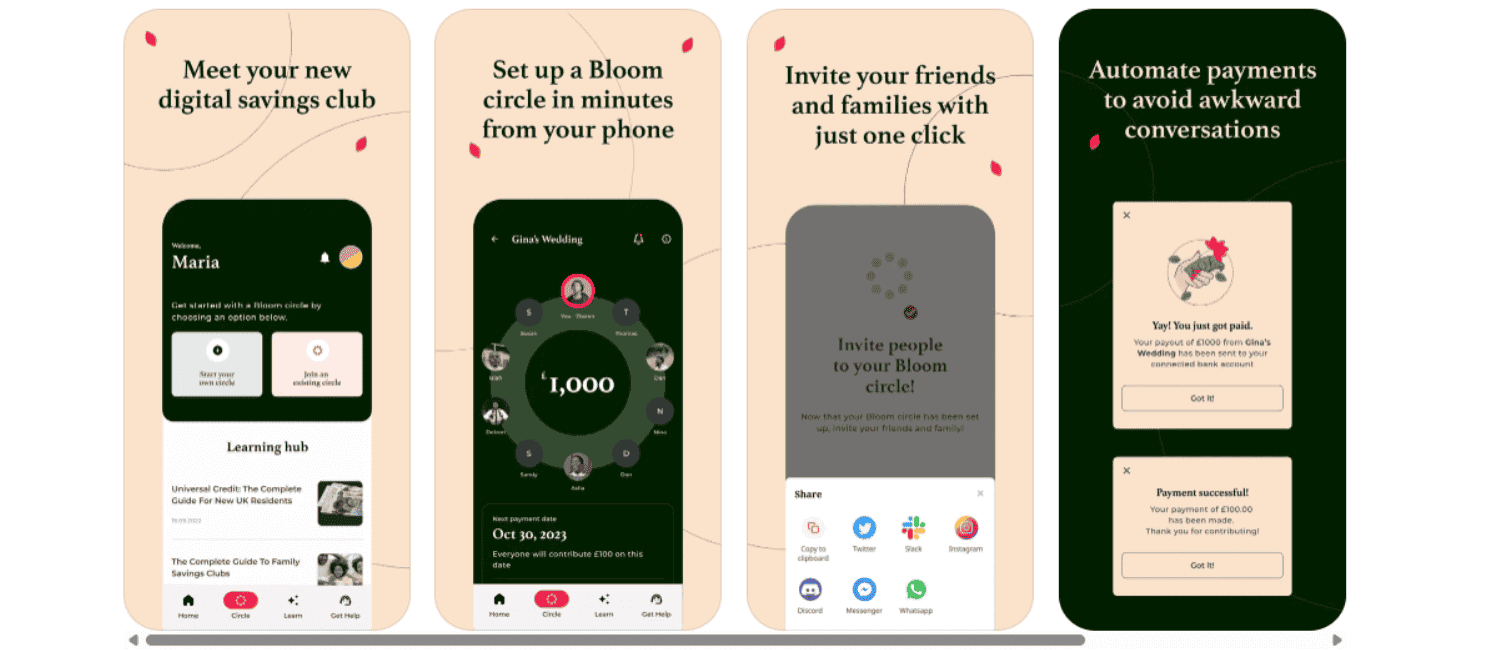

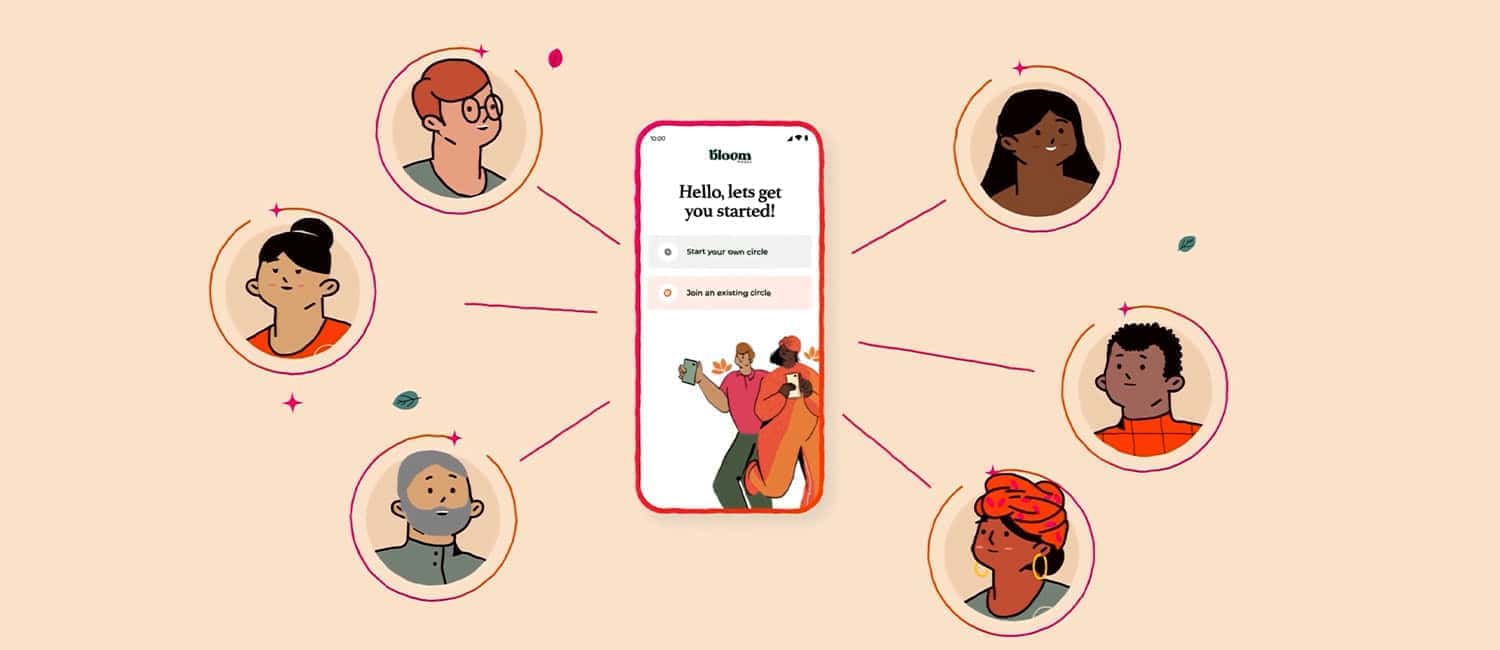

At the heart of the Bloom Money app is the Bloom Circles feature, a digital version of the community-based savings circles trusted by immigrant and diaspora communities for generations. The feature caters specifically to immigrant communities in the UK, who Mohanty describes as “providing for two households”. In the video below, she explains how Bloom Circles work in the context of global community-based savings circles:

Driven by purpose: the emotional journey to Bloom Money

Starting a business is rarely a straight line; for Nina Mohanty, the path to launching Bloom Money was no exception. It meant navigating fear, self-doubt and the risk of leaving a stable career behind. But it also meant answering a call she couldn’t ignore.

Confronting doubt and embracing conviction

Like many first-time founders, Mohanty wrestled with uncertainty before launching. But one question kept surfacing in her mind:

I kept wondering: who is building for our communities? I just felt so much conviction that this [Bloom] needed to exist in the world. And the problem was so acute that it needed to be fixed.

It’s a reminder that when conviction outweighs fear, purpose becomes one of the most powerful drivers of action – even in the face of uncertainty.

Redefining fintech for financial inclusion

Fully committing to Bloom Money required Mohanty to leave the security of a full-time job. However, she saw an even greater opportunity on the other side: the chance to create a financial system that genuinely meets the needs and reflects the lives of immigrant communities in the UK.

Mohanty believed in a better approach – one that mainstream banks often overlook – built on cultural understanding, mutual support, and community trust.

Today, over 13,000 customers across the UK use Bloom Money, and it’s reshaping what fintech can look like when designed through the lens of lived experience. The company continues to grow, recently securing $2 million in early-stage funding and featuring as Apple’s App of the Day on 16 April 2025 – two milestones that mark the company’s impact.

In her words: A conversation with Nina Mohanty

What fears or limiting beliefs did you have before registering your business, and how did you work through them?

I think a big one was: should I be the one to build this?

And, of course, the ultimate fear and limiting belief that every entrepreneur has: does anyone actually want this? And are they going to pay for it? I think there’s always going to be a bit of you as an entrepreneur that isn’t sure if it’s the right path, because there is no perfect way to build a business.

I would say I’m still working through these limiting beliefs, but it’s part of the journey and has made Bloom a more resilient and sustainable business.

What feels different about leading a business of your own?

To be the one to set the vision and the roadmap and say, here’s where we’re going, is incredibly different. It’s a massive leap for me.

The other big difference when leading a business is the constant worry about investment and investors. Luckily, we have so many wonderful investors who have come on board who get what we’re building and why.

The other difference is the constant fear of whether anyone will want to work with me. But I’ve been so blessed to have the most incredible team. Most come from immigrant backgrounds themselves. They want to work for us in pursuit of the same vision.

Starting a business can feel daunting, especially as a woman in an industry historically dominated by men. What advice would you give a woman on the verge of launching her idea?

I think the thing I have leaned on the most since starting my journey, and didn’t think about before, is my support network.

I remember the wife of one of our angel investors saying, “Nina, I only have one question for you: who is in your support group?” No one has asked me that before or since, but that was the most impactful question on this journey.

Whether you are setting up a lemonade stand, starting a coffee shop, or launching a tech company and raising millions, starting a business is so difficult.

You need a friend who will say, “Come over for a movie night and let’s just turn off our phones and watch Julia Roberts in Pretty Woman.” Or a friend that you call up and say, “I broke the Excel sheet and it’s not working. Please, can you help me?” Or someone you can rant to because you’ve had a really bad day.

I think if you’re starting on your entrepreneurial journey, you must, must, must have at least three people you can go through hell with.

Frankly, I would not still be standing if it weren’t for my support group.

What’s been your proudest moment since forming Bloom Money, and what has it taught you about resilience as a founder?

This is going to sound like a really weird moment to be proud of because it’s pretty bittersweet. But one of our engineers is leaving soon, which breaks my heart.

He comes from an immigrant background and applied for the role over two years ago. We took a chance and hired him, and he’s been an incredible engineer, employee, teammate and colleague. And he was just offered a role at Spotify.

We’re devastated to lose him, but the fact that he came to us, built up his skills, and now Spotify, which has one of the most respected engineering organisations in the world, wants to hire him is amazing. God, it’s so good.

What’s been the most surprising thing you’ve learned since launching the Bloom Money app?

That there’s so much that you don’t know as a founder. There are so many bits and pieces of fundraising and so much building to go into your product. There are so many unknowns and deadlines – like the Companies House deadlines – and it’s just a never-ending list.

So that was surprising – and is the reason for my lack of sleep.

Complete this sentence: The world needs more women business owners because…

… women build for everyone.

Women consider the whole family, the whole community, the whole village, the whole congregation.

It’s perhaps a bit of a generalisation to say that every woman cares about everyone else. But ultimately, I don’t know a single female entrepreneur who isn’t trying to make the world a better place.

Women want to create a world that they want to live in. They want to create a peaceful and beautiful world for themselves, their neighbours, their children, their neighbours’ children, and everyone around them.

Mohanty’s advice for future founders: Respond to a real-world need

What makes a great founder? According to Mohanty, it starts with deep listening. She shares her insights and learnings on building a product that’s truly helping her community.

1. Understand the people you serve

To build something that truly matters, start by deeply understanding the lives, needs and challenges of your audience. This is what it means to build a purpose-led business – you’re not only serving customers; you’re advocating for their lives and livelihoods.

Mohanty says, “If I really had to boil it down, the biggest problem we’re solving at Bloom Money is that the UK financial system is not built for newcomers. We want to be the ones to bring people into the fold and build products that understand their lifestyle, cultures and traditions.”

2. Stay close to community

Product decisions are sharper, smarter, and more meaningful when they’re grounded in real conversations and ongoing feedback from the people you serve. Mohanty credits much of Bloom Money’s progress to her strong connection with the community in Peckham, south London, where real savings circles are in motion.

“I try to be out there speaking to customers as much as possible,” Mohanty says. “We’re working towards offering so many products and services,” she adds, “but it’s our cultural understanding and the resonance of community that keeps our customers coming back over and over again.”

3. Challenge the status quo and build a better option

Just because something has always been done a certain way doesn’t mean it must stay that way – disruption can honour tradition while creating or evolving into something better.

Mohanty’s previous role at Swedish fintech giant Klarna showed her how intuitive UX, instant credit approval, and embedded financial products can change people’s thoughts about money. The experience showed that legacy systems can be reimagined rather than just gradually improved.

“Everything that we think needs to be done a certain way doesn’t actually need to be,” Mohanty says. “We know that our customers are creditworthy and are earning good money. They deserve to be treated better and have better products built for them.”

Redefining the future of fintech and inclusive finance

Bloom Money is part of a growing wave of inclusive and ethical fintech companies in the UK – alongside innovators like Algbra, Snoop, and Tully.

As Innovate Finance CEO Janine Hirt notes, “8 out of every 10 adults in the UK are regularly using at least one fintech tool, and 60% of lending by small and medium-sized enterprises across the country is being done by fintechs.”

As a result, purpose-led fintech solutions are now among the fastest-growing subsectors in the UK, with startups increasingly focused on equity, accessibility and financial wellness. And momentum continues to grow.

For founders looking to build with equity and cultural relevance in mind, the opportunity to reshape fintech and inclusive finance from the ground up has never seemed more achievable.

Maybe this is where you come in.

Movements like this develop from the grassroots, led by purpose-driven individuals who recognise what others overlook and create what their communities truly need.

Could your purpose be the beginning of something bigger?

Every movement starts with an individual who decides to take initiative.

Nina Mohanty’s journey with Bloom Money proves that lived experience, when paired with conviction, can lead to impactful change.

If you have a meaningful idea, embrace it as a valuable opportunity rather than just a fleeting dream. Give it the attention it deserves and explore the possibilities it can bring. Why not seize it and take decisive action to turn that idea into reality?

If you’re ready to take the next step, explore how to turn your vision into real impact by registering your business. At 1st Formations, we’re here to guide and support you throughout the entire process.

Join The Discussion