Zombie companies are one of the most overlooked risks businesses face. They might look upright and functioning on the surface, but underneath, they’re financially lifeless and stuck in survival mode.

In 2026, a “triple whammy” of rising interest rates, high energy prices, and the minimum wage in the UK is predicted to trigger a ‘zombie apocalypse’ (and not of the cinematic kind). According to the Resolution Foundation, thousands of underperforming businesses may collapse this year as financial pressures mount and unproductive firms reach breaking point.

Understanding the risk is essential, particularly for startups and small businesses. Once a company has fallen into “zombie status,” it can be difficult to get out of.

In this guide, we explain what zombie companies are, how to identify them early, and what you can do to avoid becoming one when business gets tough.

Key takeaways

- Zombie companies survive on debt but sacrifice growth, productivity, and innovation – trapping them in long-term stagnation.

- Zombie companies drain the wider economy by tying up capital and distorting market dynamics.

- Flat profits, rising debt, and slashed reinvestment are strong early indicators that a business may be slipping into zombie status.

What is a zombie company?

A zombie company is a business that earns just enough revenue to cover the interest on its debt. It can’t afford to pay down the principal, invest in new opportunities, or innovate.

The name is fitting: these companies shuffle along, propped up by debt and artificial support, showing signs of life but never growth.

According to a paper produced by Luca Mingarelli, Beatrice Ravanetti, Tamarah Shakir, and Jonas Wendelborn for the European Central Bank, zombie companies often manage to survive due to subsidised credit. This keeps money tied up in struggling businesses instead of going to stronger, faster-growing companies. As a result, overall productivity suffers, and healthier companies have a harder time getting the funds they need to grow.

- What decisions can directors make without shareholder consent?

- What to do if a company director dies

- How to create an employee handbook for UK startups

In the UK, over 20,000 companies with a turnover of between £10m and £500m are estimated to be “at risk” of becoming zombies or already in the process of becoming one.

It’s not just limited companies – limited liability partnerships and sole traders can face this problem as well.

What is the history of zombie companies?

The concept of a zombie company first emerged in Japan in the early 1990s, when the country went through a long period of economic stagnation. These companies were no longer healthy or profitable enough to survive in a normal economy, but they managed to stay alive because banks kept lending them money and interest rates were very low.

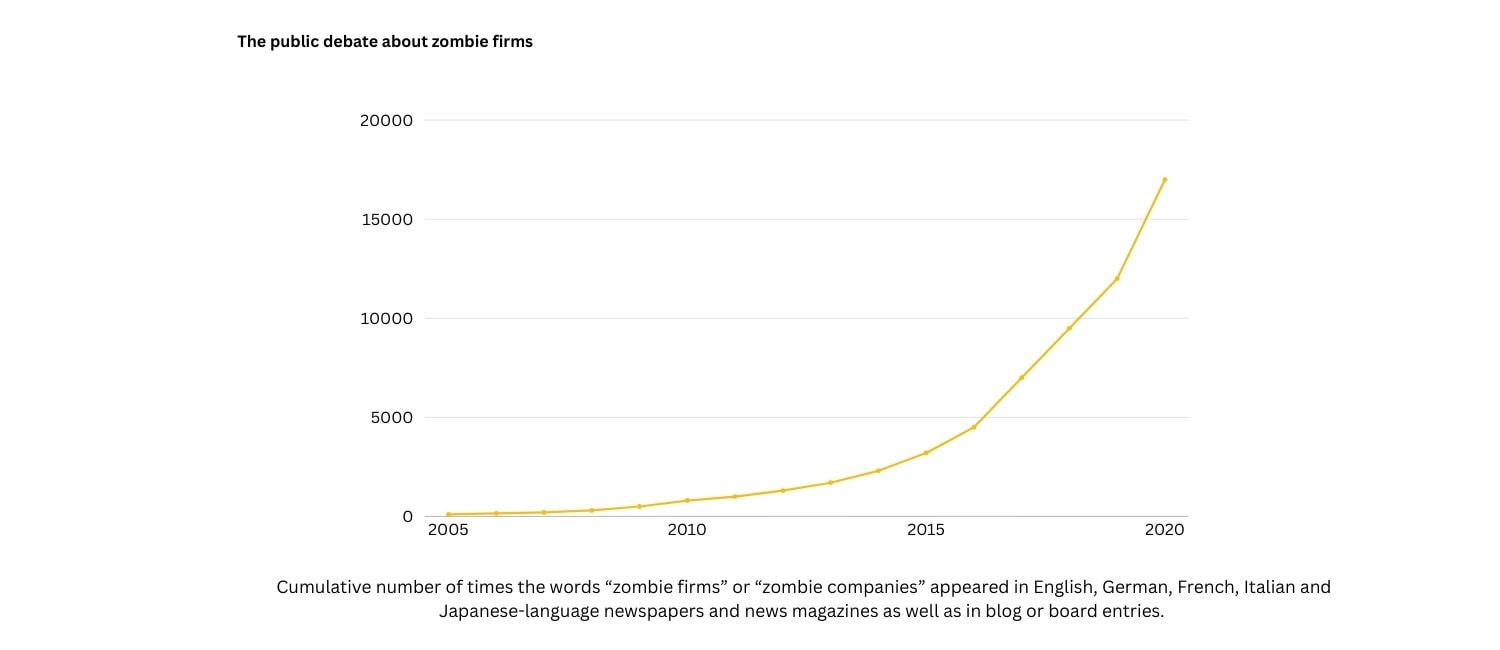

Public interest in zombie companies has grown rapidly in recent years. Mentions of “zombie firms” or “zombie companies” in global media were relatively rare until after the 2008 financial crisis. Since then, attention has steadily increased, with a sharp spike around 2020 when the COVID-19 pandemic raised fresh concerns about struggling businesses relying on government support to stay afloat.

This rise in media and public debate is shown in the graph below, which tracks mentions across newspapers, magazines, and blogs in multiple languages.

What are the traits of zombie companies?

Some typical characteristics of a zombie company include the following:

- Chronic inability to repay original debt

- Heavily reliant on external financing and support, particularly from banks or government subsidies

- Low or no business growth

- Low or no profitability, even when market conditions are more favourable

- Low productivity and stagnant innovation

Spotting these traits early is key to stopping your business from slipping into the financial coma that is being a zombie company.

What causes a business to become a zombie company?

No business sets out to become a zombie. The path is usually gradual, often marked by small compromises that accumulate into larger structural problems over time.

- Overleveraging – taking on excessive debt without sustainable cash flow.

- Poor cash flow management – inability to align income with expenses, especially in volatile markets.

- Market stagnation or disruption – operating in sectors where demand is declining or digital alternatives are taking over.

- Outdated business models – failure to evolve, such as resisting tech or ignoring modern consumer needs, is a common final nail in the coffin.

Examples of zombie companies

It’s difficult to get data on companies that have zombie status. As the BBC’s Hugh Pym nicely puts it, finding a company that’s prepared to own up to zombie status is not easy.

Although some industries are more susceptible to this phenomenon, like real estate and hospitality, it can happen anywhere.

Commonly cited examples of zombie companies (or those that appear to show traits associated with zombie status, like stagnation) include Air Berlin, JCPenney, and Barnes & Noble. Behind the corporate mask, these companies have shown clear signs of zombification.

How do zombie companies survive?

Zombie companies manage to survive through financial mechanisms that keep them operational without addressing their fundamental challenges.

Low interest rates allow businesses to refinance debt repeatedly, avoiding immediate collapse but failing to resolve deeper issues. Some can access government bailouts or cheap credit during economic downturns, providing them with temporary relief. Others negotiate debt restructuring arrangements where they gain more lenient repayment terms.

While these tactics can extend a company’s life, they come at a cost. A prolonged reliance on external support locks businesses into a cycle of survival. The cost? Innovation stalls. Teams stagnate. Creativity dies. Expansion into new markets is hindered. All in the name of keeping the business “alive”.

Why are zombie companies harmful to the economy?

At first glance, a zombie company may seem like just another struggling business. On their own, they might not necessarily be a problem. But when there are too many that exist, they can have a serious and lasting impact on the wider UK economy.

Capital is misallocated

Zombie companies tie up funding that could be better used elsewhere. Banks, investors and lenders often keep these firms afloat despite poor performance, diverting capital away from innovative or fast-growing businesses.

Competition becomes distorted

Zombie companies often undercut prices, not to compete, but rather to just survive. This forces healthier competitors to fight on uneven ground, especially startups, who must match unsustainable prices while trying to grow. In a nutshell, markets overrun with zombies leave less room for the living (strong, viable businesses) and stifle growth.

Productivity and innovation decline

Zombie companies often stop investing in staff development, technology, or product improvement. Over time, entire sectors can stagnate. Without progress, productivity weakens, and the ripple effects can be felt economy-wide.

Why UK SMEs are at risk of zombification in 2026

While larger organisations may have more buffers to weather economic shifts, UK small and medium-sized enterprises (SMEs) face a significantly higher risk of zombification in 2026. Several challenges come into play: inflation, ongoing high energy costs, minimum wage increases, and a cautious investment climate. According to Vicky Pryce, Chair of the BCC Economic Advisory Council:

Businesses will be steering through choppy waters once again next year after a Budget that lacked the growth measures so desperately needed. Getting inflation back down towards the Bank’s 2% target is good news, but that masks the continuing cost pressures for businesses.

Although inflation is easing, Pryce stresses that many SMEs are still grappling with cost pressures as interest rates remain high and significant cuts are far from guaranteed. With unemployment expected to rise and consumer spending likely to slow, SMEs – already tighter on cash flow and often reliant on short-term borrowing – are more exposed to thin margins, stagnation, and even collapse. These conditions make it harder to reinvest and innovate, two vital defences against slipping into zombie status.

How to identify a zombie company: Early warning signs

Zombie companies don’t emerge overnight. The decline from a viable, growing business to one that’s barely surviving is usually slow and subtle – especially when daily operations still appear stable.

So, what are the early warning signs of your company becoming a zombie?

- Rising debt to cover operations – frequent borrowing just to stay afloat signals a reliance on credit rather than sustainable income.

- Flat or falling profits – revenue might be steady, but rising costs or shrinking margins erode profitability, with no clear plan for reversal.

- Tight, unreliable cash flow – delays in supplier payments or payroll issues suggest the business lacks financial breathing room.

- Lack of reinvestment – cutting back on marketing, innovation, or staff training indicates a business stuck in survival mode.

These signs don’t confirm a business is a zombie, but they do suggest it may be drifting in that direction and action is needed.

Can a zombie company recover?

The good news is that it’s often possible for a zombie company to recover. However, doing so takes decisive action, starting with an honest assessment of the underlying challenges. For some, it may also serve as a warning to act early and avoid becoming a zombie in the first place.

Here’s how to avoid zombification, or claw your way back if you’re already stuck in survival mode:

| Issue | What you can do |

| Struggling to keep up with debt repayments | Renegotiate loan terms or refinance debt to relieve short-term pressure and improve cash flow. |

| Products or services not driving growth | Evaluate product performance and cut offerings that no longer meet market needs. |

| Costs and overheads outweighing revenue | Streamline operations to match current income. Explore commonly overlooked money-saving tips to help reduce costs. |

| Declining customer engagement or rising churn | Revitalise your brand, adopt digital tools, or reposition your offer to meet changing customer expectations. |

| Persistent tax arrears | Agree a Time to Pay arrangement with HMRC to spread tax repayments over affordable instalments. |

| Ongoing creditor pressure | Use a Company Voluntary Arrangement (CVA) to negotiate debt while continuing to trade. |

| No clear strategy or leadership focus | Bring in turnaround specialists or restructuring advisors for fresh insight and guidance. Revisit your business plan, as well. |

Delta Airlines: An example of zombie company recovery

Like many airlines, Delta Airlines became one of the walking dead during the COVID-19 pandemic, when global air travel came to a near standstill. Its revenues plummeted, debt soared, and the company became heavily reliant on emergency financing, government support, and cost-cutting measures just to stay operational, giving some analysts cause to claim it had become a zombie.

Yet, through fleet cuts, streamlined operations, debt restructuring, and strategic route shift rebuilding, the company staged a comeback.

Today, Delta has regained profitability and customer trust. Its success shows even the gravest situations can be reversed with clear-eyed strategy and a willingness to kill off failing ideas.

Get professional help to avoid becoming a zombie

Zombie companies are a problem not just for the businesses themselves, but for the wider economy. As we’ve explored, slipping into zombie status is often a gradual process – but it’s entirely avoidable with the right insight and timely action.

If your business is financially stuck, time is key. Delaying action only feeds the cycle. Seek expert advice, such as speaking to a turnaround specialist, to identify the root cause, safeguard what’s working, and set a clear path forward.

Or, if you’re just starting out and planning to register a UK company, make sure your business plan is zombie-proof from day one. Knowing the risks can help you build smarter, avoid common pitfalls, and set your business up for long-term success.

Join The Discussion