You’ve probably already read somewhere that a relevant legal entity (RLE) is a company or organisation that has significant control or influence over your business. But that definition alone is only half the story. There are specific conditions under UK law that separate any old company that has a say in how your business is run, from an actual RLE you need to record and report. That’s why we’ve put together this guide to help you fully get to grips with what an RLE is, how to identify one, what to do next, and how to comply with your ongoing recording and reporting responsibilities.

Key takeaways

- A relevant legal entity (RLE) is a company or organisation that has significant control over your business and meets the same conditions as a PSC if it were an individual.

- A legal entity is relevant if it’s subject to an appropriate disclosure regime (for example, it must disclose its own controllers to Companies House).

- An RLE is registrable when it’s the first RLE in the ownership chain above your business.

- You have 28 days to notify Companies House when an RLE becomes registrable.

- You must keep Companies House updated if an RLE’s details change or they’re no longer an RLE.

What is a relevant legal entity?

An RLE is a company or organisation that has significant control or influence over a business. It satisfies the same conditions that would qualify it as a PSC if it were an individual. A business must notify Companies House of all the RLEs it has. This is because the business is subject to a disclosure regime.

A company can only be listed as an RLE if it is also subject to a disclosure regime. If not, you need to look through the company to find the individuals who are really in control and, if they qualify, list them as PSCs instead.

- Companies House identity verification: Guidance & requirements

- A guide to the Register of People with Significant Control (PSC)

- How to remove a PSC from a limited company or LLP

Understanding the definition of a relevant legal entity (RLE) is like building a piece of flatpack furniture. You first need to figure out what each of the parts are before you can start fitting them together.

In this analogy, the parts are a few key terms:

- Person with significant control (PSC): an individual who has significant control or influence over a business, usually because they have more than 25% shares or voting rights.

- PSC register: a list of PSCs that every UK incorporated business must file with Companies House alongside their confirmation statement.

- Disclosure regime: a transparency framework that requires businesses to identify their PSCs, tell Companies House who they are, and for these details (in addition to other key company information) to be made publicly available.

How to identify a relevant legal entity

For a company or organisation to satisfy the same conditions that would qualify it as a PSC if it were an individual, one or more of the following must be true:

- It holds more than 25% of the shares in the business

- Check: the cap table and register of members, including any parent-company holding.

- It holds more than 25% of the voting rights

- Check: share classes, voting provisions in the articles, and any agreement changing voting rights.

- It has the power to appoint or remove the majority of directors

- Check: the articles and shareholders’ agreement, including any rights attached to specific shares or investor consents.

- It otherwise can or does significantly influence or control the business

- Check: reserved matters, veto rights, consent requirements or arrangements giving ongoing management control.

- It has significant influence or control over the activities of a trust or firm that’s not a legal entity, but would itself satisfy any of the other conditions above if it were an individual.

If you’re unsure, watch this video for detailed guidance about identifying PSCs.

Source: GOV.UK – Companies House guidance on PSCs

Conditions that qualify a legal entity as relevant

For the company or organisation (legal entity) to be treated as relevant to the business, it must also be subject to a disclosure regime. In practice, that means meeting at least one of these conditions:

- It must identify who controls it and submit those details to the central register at Companies House.

- Its voting shares are traded on an approved regulated market in the UK or EEA, or on certain specified markets in Switzerland, the USA, Japan, or Israel.

What makes an RLE registrable in the ownership chain?

Once you’ve confirmed a legal entity is relevant, the next question is whether it’s registrable. Registrable simply means: is this the first relevant legal entity you hit when you trace ownership upwards from your company? If it is, that’s the RLE you record and report.

Think of it like following a trail. You start with your company, look at who owns it, then look at who owns them, and so on. You stop at the first entity that meets both tests you’ve already covered:

- It meets at least one of the PSC control conditions, and

- It qualifies as relevant by (subject to a disclosure regime)

Registrable RLE checklist

If we put all of that together, you get a quick and easy checklist to confirm that a company or organisation is a registrable RLE:

- The entity is a company or organisation (not an individual)

- It meets at least one of the PSC control conditions

- The entity is subject to a disclosure regime (it’s relevant)

- It’s the first RLE in the ownership chain

Here are a few examples:

Example 1: Shares

Your UK company is owned 60% by another UK limited company. That UK company meets at least 1 of the PSC conditions (shares, voting rights, and appointment and removal of a majority of the directors) and is subject to a disclosure regime (it’s registered at Companies House), so it’s an RLE. Because it’s the first RLE above you, it’s registrable and should be recorded and reported.

Example 2: Voting rights

A UK LLP only holds 20% of the shares in your UK limited company but has 30% of the voting rights. It meets the voting rights condition and is within the disclosure regime rules (it’s registered at Companies House), so it’s an RLE. If it’s the first RLE in the chain, it’s registrable.

Example 3: Multiple RLEs

Your UK company is owned 40% by UK Company A and 30% by UK Company B. Both meet the shares condition and are subject to a disclosure regime. If there is no closer RLE above either of them in their respective chains, both A and B are registrable RLEs for your company.

Example 4: Board control

A UK company only holds 15% of shares but has the right to appoint/remove a majority of directors. It meets the board control condition, so it can be an RLE.

Example 5: Other influence/control

A UK company holds a minority stake but has veto rights over budgets, business plans, issuing shares, or hiring/firing senior management. That can amount to significant influence or control. If it’s the first relevant legal entity in the chain, it may be the registrable RLE.

Visit GOV.UK for more examples that illustrate relevance and registrability.

Overseas entities: What changes?

Overseas companies often fall down at the relevance step. If an overseas entity is not subject to a disclosure regime (for example, it is not registered at Companies House), it can’t be your registrable RLE. In that case, you’ll usually need to look through it until you find either:

- An entity that does qualify as relevant (and is the first one), or

- The individual who has influence/control (to record as a PSC)

Here are a few overseas examples:

Example 1: Disclosure regime

Your UK company is owned 100% by an overseas company that isn’t subject to a disclosure regime. It isn’t an RLE, so you look through it to find the individual who controls the structure (and record them as PSCs if they qualify).

Example 2: Approved market

Your UK company is owned 100% by an overseas company whose voting shares trade on an approved market, so it meets the disclosure regime test. If it’s the first RLE in the chain, record it as the registrable RLE.

Example 3: UK ownership

Your business is owned by a private overseas holding company that isn’t subject to a disclosure regime, but that holding company is owned by a UK company that is. Look through the overseas company and record the UK company as the first registrable RLE.

Recording and reporting a relevant legal entity

Once you’ve identified a new registrable RLE, you need to notify Companies House within 28 days.

You’ll need the following RLE details to hand:

- Company name and registered address

- Legal form (e.g. LLP, limited company)

- Governing law (e.g. Companies Act 2006)

- Public register and registration number

- Date it became registrable

- Nature of control (e.g. more than 25% shares)

Remember: recording and reporting a registrable RLE is a quick and event-driven process – not something to leave until your next confirmation statement. The clock starts ticking the day you identify a registrable RLE.

How to notify Companies House about a new RLE

Online

The quickest way to notify Companies House about a new RLE is to use their online WebFiling service. Recent changes mean you’ll need to sign in using your GOV.UK One Login (if you don’t have one already, you’ll have the option to create one).

If you’re a 1st Formations customer, simply log in to your account and tell Companies House about a new RLE using our Online Company Manager. Not yet a 1st Formations customer? Learn more about our Hassle-Free Compliance Service.

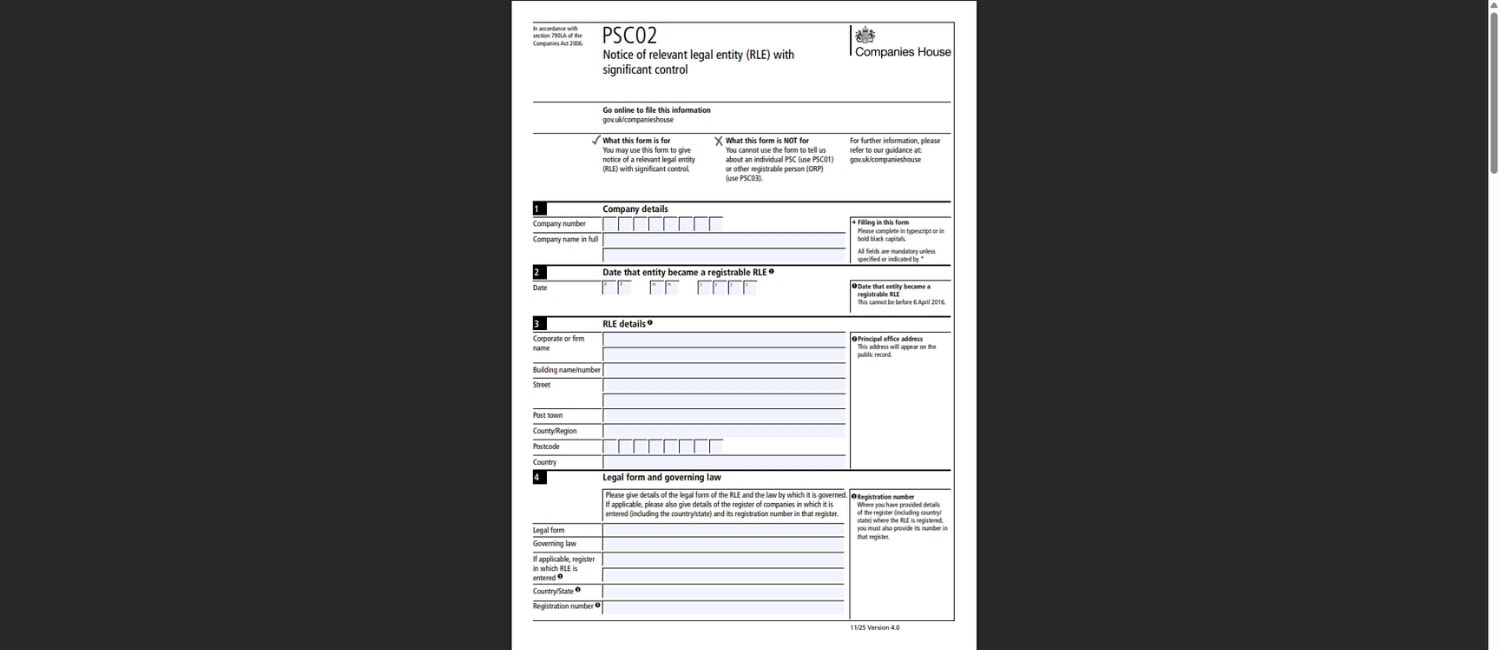

By post

You can also print and post a paper PSC02 form, but this route takes longer and is subject to processing delays. If you choose this route, send off your form well ahead of the deadline.

Visit GOV.UK for more detailed 2026 guidance.

Practical tips and common pitfalls

Even with a solid understanding of the rules, real-world situations – such as restructures and investment rounds – can complicate RLE reporting. We’ve put together some practical tips and a few common pitfalls to look out for.

Base relevance on evidence, not assumptions

Keep a short note (and supporting proof) showing why the entity is subject to an appropriate disclosure regime, especially for overseas entities or group structures. This makes future reviews and queries much easier.

Make sure your wording is aligned

Errors occur when your internal PSC register entry and Companies House update describe control differently (for example, voting rights vs. shares, or multiple conditions). What you record and what you report should be one in the same.

Watch for control held through agreements

It’s easy to miss that reserved matters, vetoes, or director appointment rights in a shareholders’ agreement can meet the significant influence/control condition, even where the equity stake is below 25%. Flag and review these clauses whenever you onboard investors or amend the agreement.

Use “date became registrable” consistently

In restructures and share transfers, teams often use the completion date in one place and the effective date in another. Set a single effective date internally (with a short rationale), then use it for the PSC register and the Companies House update.

Build a trigger checklist into your transaction workflow

Share allotments, share transfers, new share classes, amendments to articles, new investor rights, or changes to board appointment rights should automatically prompt a PSC/RLE review. This reduces the risk of missing event-driven updates.

Comply with ongoing RLE reporting responsibilities

Don’t just file and forget – you must keep your PSC register and Companies House up to date. If an RLE’s details change, use the WebFiling service or form PSC05 to tell Companies House within 14 days. You also have 14 days to record and report (online or PSC07 by post) when a company or organisation is no longer an RLE.

Access expert support

Understanding and identifying an RLE is crucial for ensuring compliance. An RLE can significantly influence your business and must meet specific conditions to be registered. By actively monitoring ownership structures and keeping accurate records, you can fulfil your legal obligations while maintaining transparency within your organisation.

Remember, timely reporting to Companies House is essential, so stay vigilant about any changes in control or ownership. At 1st Formations, we appreciate that running your business while meeting numerous legal and admin duties can be challenging. That’s why we offer a range of company services and resources to help make things easier.

Join The Discussion